The Financial Basics Most People Were Never Actually Taught

Have you ever found yourself thinking:

“I wish someone had taught me this when I was younger.”

If so, you’re not alone.

(more…)

Have you ever found yourself thinking:

“I wish someone had taught me this when I was younger.”

If so, you’re not alone.

(more…)

When people think about financial planning, they often picture a fairly straightforward situation.

A steady paycheque. A mortgage. Monthly bills. Retirement savings.

For many farm families, life doesn’t look like that. Farming is more than a career. It’s a business, a lifestyle, a family legacy, and often the result of generations of hard work.

That’s why financial planning for farm families is different.

(more…)

Recently, my partner and I started watching The Madison with Kurt Russell.

In the first episode, there’s a story that really stuck with me.

He talks about taking his family to an all-inclusive resort and noticing that most of the people there were about twenty years older than they were. The point wasn’t about age itself. It was about something much deeper.

(more…)

By the time June arrives, the year often starts to feel a little more real financially.

The excitement and motivation that comes with January goals has settled. Markets have moved. Life may have shifted. And for many people, the first half of the year has gone differently than expected — sometimes in good ways, sometimes not.

That’s why June can be an ideal time to pause and reassess your portfolio and overall financial plan.

Not from a place of panic or urgency.

But from a place of clarity.

At YourStyle Financial, portfolio reviews are less about reacting to headlines and more about making sure your plan still reflects what’s important to you.

What Portfolio Rebalancing Actually Means

Portfolio rebalancing sounds technical, but the concept is relatively simple.

Over time, different investments grow at different rates. As markets move, your portfolio can slowly drift away from the original balance and risk level you intended.

For example:

Rebalancing is the process of reviewing and adjusting those allocations to bring things back in line with your long-term goals and comfort level.

It’s not about trying to predict markets.

It’s about maintaining alignment.

Why June Is a Natural Time to Review Things

Mid-year reviews can be valuable because they create space to reassess before the year moves too far ahead.

By June, people often have a clearer picture of:

Sometimes the review confirms things are on track. Other times, it reveals opportunities to simplify, adjust, or improve.

Either outcome is helpful.

Financial planning works best when it’s ongoing and adaptable — not something revisited only when markets become stressful.

Reassessing More Than Just Investments

A portfolio review is also an opportunity to step back and ask broader questions.

Good financial planning looks beyond performance numbers.

It considers how your finances connect to your lifestyle, your priorities, and your sense of stability moving forward.

Avoiding Emotional Decision-Making

One of the challenges investors face is the temptation to react emotionally when markets move.

That’s understandable. Headlines are designed to create urgency and uncertainty.

But long-term financial planning is rarely improved by short-term reactions.

A thoughtful reassessment creates space to:

For many people, that perspective is far more valuable than trying to constantly “outguess” the market.

Planning That Fits Your Comfort Level

Not everyone approaches investing the same way.

Some people want detailed conversations and active involvement. Others prefer a quieter, more simplified approach.

There’s no right or wrong way to engage with financial planning.

The important thing is that your portfolio and overall plan reflect:

At YourStyle Financial, the process is designed to feel approachable and collaborative — not overwhelming.

What’s Important to You?

At the centre of every portfolio review is a simple question:

What’s important to you?

Because financial planning isn’t just about investment returns. It’s about supporting the life you’re building and making sure your plan continues to reflect what matters most.

June can be a good reminder that financial planning doesn’t need to happen only during major life events or market uncertainty.

Sometimes it’s simply about taking the time to reassess thoughtfully.

If it’s been a while since you reviewed your portfolio or financial plan, this may be a good opportunity to check in and make sure things still feel aligned with where you’re headed.

If you’d like to have a conversation about your portfolio, your goals, or where things are headed, you’re always welcome to reach out.

— Sean

There’s a phrase I hear often lately:

“I want to save… but everything already feels expensive.”

And honestly, that feeling is understandable.

Between groceries, housing costs, interest rates, childcare, transportation, and everyday life, many people feel stretched thin — even when they’re working hard and doing everything “right.”

Because of that, saving money can sometimes feel overwhelming. Or impossible.

But I want to gently offer a different perspective:

Saving doesn’t have to start big to matter.

At YourStyle Financial, we often remind people that financial progress is usually built through small, consistent steps — not dramatic overnight changes.

The Pressure to “Do More”

One of the biggest reasons people avoid saving is because they think they need to start with large amounts.

A few hundred dollars a month.

A perfectly organized budget.

A full financial plan already figured out.

But that pressure can actually stop people from starting at all.

The truth is:

Even setting aside a modest amount regularly can begin building confidence alongside savings.

Start With an Emergency Fund

Before focusing heavily on investing, many people benefit from first building a small emergency fund.

Think of it as a financial buffer zone for when life gets difficult.

Unexpected car repairs, appliance breakdowns, medical expenses, reduced work hours — these things happen. And when there’s no cushion in place, even small emergencies can quickly turn into stress or debt.

An emergency fund doesn’t need to be huge to be helpful.

Even starting with a small goal can create peace of mind and breathing room over time.

Pay Yourself First

One of the simplest — and most effective — saving strategies is something called “pay yourself first.”

Instead of waiting until the end of the month to save whatever might be left over, you move money into savings as soon as you get paid.

Why does this matter?

Because for most people, there often isn’t leftover money at the end of the month.

Automating savings, even in small amounts, helps remove the pressure of constantly making the decision manually.

That might look like:

Consistency is usually more important than the amount itself.

Track Where Your Money Is Actually Going

Sometimes the challenge isn’t income alone — it’s money quietly leaving without us noticing.

Subscription services are a great example.

Streaming platforms, unused memberships, apps, delivery services, or recurring charges can slowly add up over time, especially when multiple small expenses are combined.

Taking time to review your monthly spending can help identify:

This isn’t about guilt or restriction.

It’s simply about making sure your money is going where you actually want it to go.

Why a TFSA Can Be a Great Starting Point

For many Canadians, a Tax-Free Savings Account (TFSA) is one of the most flexible ways to begin saving.

A TFSA allows:

That flexibility matters when life feels unpredictable.

Whether you’re saving for:

A TFSA can create room for future choices without locking your money away.

Saving Is Emotional Too

This part matters more than most people realize.

Saving money isn’t only about math.

It’s also about:

Even small savings can create emotional breathing room.

And sometimes, that’s where the biggest shift begins.

You Don’t Need to Be Perfect to Start

One of the most common things I hear is:

“I should have started sooner.”

Maybe. But that thought doesn’t help you move forward today.

What matters most is simply beginning from where you are now.

No judgment.

No perfection required.

No “right” timeline.

Just thoughtful steps that fit your life.

A Simple Question to Ask Yourself

Instead of asking:

“How much should I be saving?”

Try asking:

“What amount could I save consistently without creating more pressure?”

That answer is often a much healthier place to begin.

And over time, small consistent habits can grow into something meaningful.

If you’d like help creating a plan that feels realistic for your life today, I’m always happy to have a conversation.

— Samantha

There’s a common misconception that financial planning is only for people who already “have money.”

People often assume they need:

The truth is, most people don’t start there.

And honestly, waiting until everything feels perfect is usually what delays people from getting started in the first place.

Financial Planning Isn’t About Being Rich

One of the biggest things I’ve noticed in conversations with people my age is how many feel behind financially.

Housing feels expensive.

Groceries are expensive.

Life is expensive.

A lot of people feel like they’re just trying to keep up — and because of that, financial planning starts to feel like something for “later.”

But financial planning isn’t about being wealthy.

It’s about having a direction.

Even small steps can create meaningful momentum over time.

Starting Small Still Matters

One of the biggest advantages anyone can have financially is simply starting earlier.

Not perfectly.

Not aggressively.

Just earlier.

Even something as simple as:

can make a much bigger difference over time than people realize.

The goal isn’t to do everything at once.

It’s to start building habits and structure before life becomes more complicated.

Most People Feel Like They “Should Know More”

This is another thing I hear often:

“I feel like I should understand this already.”

But personal finance isn’t something most people are formally taught.

A lot of people are trying to learn:

all at the same time — while also managing everyday life.

It’s okay not to know everything.

Financial planning should feel like a conversation, not a test.

Planning Looks Different for Everyone

There’s no single “right” starting point.

For some people, planning means:

For others, it’s:

Especially in Manitoba, and particularly in farming or small business environments, finances often don’t look neat and predictable. Income can fluctuate. Priorities change. Life changes.

That’s why good planning should be flexible and personal — not one-size-fits-all.

The Biggest Mistake Is Usually Waiting Too Long

A lot of people delay financial decisions because they feel like they need:

before getting started.

But time is one of the most valuable financial tools available.

The earlier someone begins learning, saving, or investing — even modestly — the more options they usually have later.

You don’t need to have everything figured out to take the first step.

Final Thoughts

Financial planning isn’t about looking wealthy or having a perfect situation.

It’s about understanding where you are today and making decisions that support where you want to go.

That might mean starting small.

It might mean asking questions.

It might simply mean having a conversation.

And that’s okay.

If you’ve been putting off financial planning because you feel like you’re “not there yet,” you’re probably more ready than you think. Let’s chat about that.

A Question More Winnipeg Families Are Asking

“Should we help our kids now… or leave it to them later?”

It’s a conversation we’re having more and more with clients here in Winnipeg.

And it makes sense.

Many parents and grandparents are in a position where they’ve built enough to feel secure—but they’re looking at the next generation facing higher housing costs, student debt, and financial pressure earlier in life.

So the question becomes:

Does it make more sense to give while you’re here to see the impact—or pass it on later through your estate?

There’s No One-Size-Fits-All Answer

Just like most things in financial planning, the answer depends on your situation.

But there is one principle we always come back to first:

You need to be financially secure before you gift.

That means:

Once that foundation is in place, gifting can become a very meaningful and strategic decision.

Why More Families Are Choosing to Gift Now

When it fits the plan, gifting during your lifetime can create real impact—not just financially, but emotionally as well.

Here are some of the most common reasons we see:

Helping Pay Down or Eliminate Debt

Reducing or eliminating high-interest debt—like credit cards or personal loans—can dramatically improve someone’s financial position.

It’s not just about the numbers.

It’s about reducing stress and creating stability.

Supporting a First Home Purchase

For many younger families, coming up with a down payment is one of the biggest barriers to homeownership.

A well-timed gift can:

Investing in Education for Grandchildren

Contributing to education savings (like RESPs) can have long-term benefits.

You’re not just giving money—you’re helping create opportunities.

Reducing Future Estate Complexity and Taxes

Strategic gifting can sometimes reduce the size of your estate, which may help minimize future tax implications and simplify the estate administration process.

This isn’t about avoiding responsibility—it’s about planning intentionally.

The Emotional Side of Gifting

This part often gets overlooked.

When you gift during your lifetime, you get to:

For many people, that’s just as valuable as the financial benefit.

When It May Make Sense to Wait

Gifting isn’t always the right move right away.

It may make sense to hold off if:

That’s why PLANNING matters.

Because once a gift is given, it’s typically irrevocable.

How We Approach This at YourStyle

At YourStyle Financial, we don’t look at gifting in isolation.

We look at the full picture:

Because gifting isn’t just about generosity—it’s about alignment with your overall plan.

Live for Today. Plan for Tomorrow.

You’ve worked hard to build what you have.

The question isn’t just how much you leave behind—it’s how and when it makes the most impact.

And sometimes, that means giving when it matters most.

Let’s Talk It Through

If you’ve been thinking about helping your children or grandchildren now—or wondering how it fits into your overall plan—we can map it out together.

Clear, thoughtful planning helps you:

Connect with YourStyle Financial to start the conversation.

Because what you’ve built isn’t just about you.

It’s about what matters most to you.

— Doug

For many people, financial planning feels like something they should do “once things are more organized.”

Maybe after:

Until then, it’s easy to feel like you’re not quite ready.

But the reality is, most people don’t begin financial planning because they have everything figured out. They begin because they want clarity about what comes next.

And that’s exactly where good financial planning should start.

Financial Planning Isn’t About Being Perfect

One of the biggest misconceptions about working with a financial advisor is the idea that you need to arrive fully prepared.

You don’t.

You don’t need:

Financial planning isn’t about proving you’ve done everything right. It’s about understanding where you are today and creating a path forward that supports what’s important to you.

That process starts with a conversation — not perfection.

Why So Many People Delay Financial Planning

For some, it’s uncertainty.

For others, it’s intimidation.

Many people worry they’ll feel judged for:

Others simply feel overwhelmed by the amount of information online and don’t know where to begin.

These concerns are more common than you might think.

The truth is, financial planning should reduce stress — not add to it.

The First Step Is Often Simpler Than Expected

At YourStyle Financial, planning begins by understanding the person, not just the numbers.

That means conversations around:

There’s no expectation to have everything mapped out before reaching out.

Often, clarity develops gradually through thoughtful conversations and small, manageable steps.

Progress Matters More Than Timing

Many people assume they’ve waited too long to start planning.

In reality, building momentum is often more important than starting perfectly.

Small decisions made consistently over time can create meaningful long-term change:

Financial planning doesn’t need to happen all at once.

It’s a process of building confidence and understanding over time.

A Comfortable Approach to Planning

Everyone approaches financial decisions differently.

Some people want detailed explanations and regular meetings. Others prefer a quieter, more gradual process with time to reflect before making decisions.

There’s no single “correct” way to approach planning.

A good financial advisor understands that comfort matters. The process should feel approachable, collaborative, and aligned with your personality — not rushed or overwhelming.

Especially for individuals or couples who are naturally more introverted or thoughtful, having a calm and supportive planning experience can make all the difference.

What’s Important to You?

At the centre of financial planning is a simple but important question:

What’s important to you?

Not what someone else is doing.

Not what social media says you should prioritize.

Not what feels urgent in the moment.

Just you.

Whether your focus is:

Financial planning should support those goals in a way that feels manageable and meaningful.

You Can Start Before You Feel “Ready”

Most people don’t begin financial planning because they suddenly feel fully prepared.

They begin because they want guidance, clarity, and a better understanding of where they’re headed.

You don’t need to have everything figured out before starting that conversation.

If you’ve been thinking about planning but weren’t sure if it was the “right time,” that’s okay.

Sometimes the best first step is simply having a place to start.

If you’d like to talk through your situation in a calm, no-pressure environment, you’re always welcome to reach out.

– Sean

It’s something I hear often:

“At least my money is safe in the bank.”

And I understand where that comes from.

There’s comfort in knowing your savings aren’t going up and down with the markets.

But what’s often missed is this:

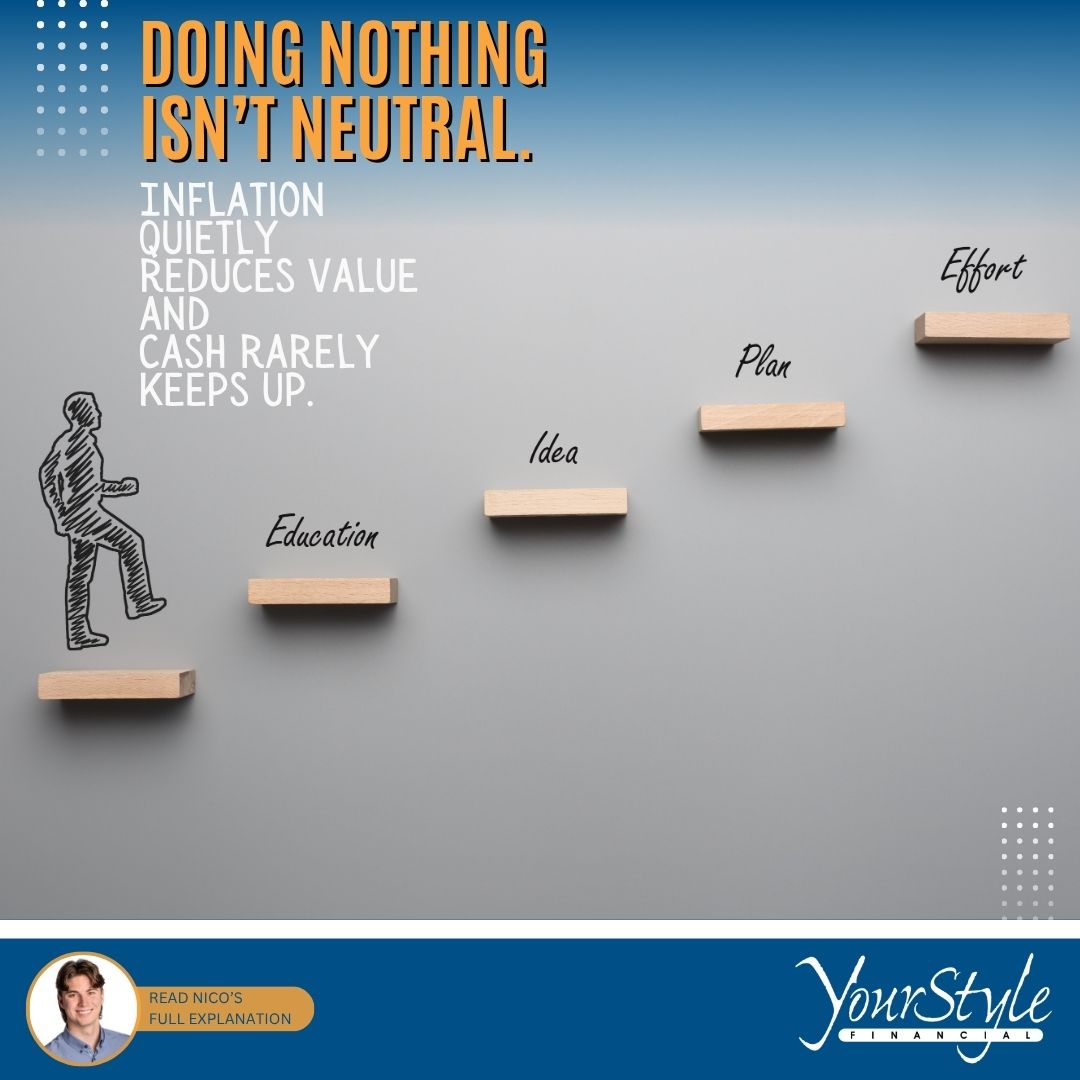

Doing nothing with your money isn’t neutral.

Over time, it can quietly cost you more than you think.

Inflation Is Always Working in the Background

Even when inflation feels “low” — say 2–3% — it’s still reducing what your money can actually do for you over time.

A simple way to think about it:

Nothing dramatic happens overnight.

But over years, the difference becomes meaningful.

The Opportunity Cost of Staying in Cash

Keeping money in a savings account might feel like the safest choice — but there’s a trade-off.

Historically:

That gap matters more than most people realize.

Here’s a simple example:

That’s not about taking unnecessary risk — it’s about understanding what happens when money doesn’t grow.

Time Is the Most Valuable Asset You Have

One of the biggest advantages anyone can have financially is simply starting earlier.

Even small amounts can make a significant difference over time.

To put this into perspective, here’s an example assuming a 7% annual rate of return over the long term:

Example:

Scenario A: Start Small, Then Increase Later

Results:

Scenario B: Wait, Then Invest More

Results:

These are hypothetical examples for illustration purposes, and actual returns will vary.

Even though the contributions are similar, the earlier start leads to a noticeably different outcome.

Not because of how much was invested — but because of time.

It’s Not About Taking Big Risks

This isn’t about putting everything into the market or making aggressive decisions.

It’s about balance.

For many people, the biggest risk isn’t volatility — it’s falling behind quietly without realizing it.

Final Thoughts

If your money is sitting in a savings account, you’re not doing anything wrong.

But it’s worth asking:

Is this working as well as it could for me?

Financial planning isn’t about pressure or quick decisions.

It’s about understanding your options and making choices that feel right for you.

If you ever want to talk it through — even just as a second opinion — I’m always happy to listen.

For many people, financial planning comes with a quiet hesitation.

Not because they don’t care — but because they’re unsure if they’re “ready.”

You might feel like:

Those thoughts are more common than you might expect.

But financial planning isn’t about where you “should” be. It’s about where you are — and what matters to you moving forward.

There’s No Perfect Starting Point

One of the most common misconceptions about financial planning is that you need to have everything in order before you begin.

In reality, there is no perfect starting point.

Some people come in with detailed plans and spreadsheets. Others come in with questions, uncertainty, or simply a sense that it’s time to start thinking about things differently.

Both are completely valid.

Financial planning should begin with understanding — not expectations.

A Different Kind of Conversation

At YourStyle Financial, the process doesn’t start with numbers.

It starts with a conversation.

There’s no pressure to have the “right” answers.

The goal is to create a space where you can talk openly, without feeling judged or evaluated. From there, clarity tends to follow naturally.

Progress Over Perfection

It’s easy to feel like financial decisions need to be perfect.

But most of the time, progress matters more.

Small, thoughtful steps taken consistently tend to have a greater impact than trying to get everything exactly right all at once.

Financial planning isn’t about fixing the past. It’s about creating a path forward that feels steady and manageable.

A Pace That Feels Comfortable

Everyone approaches planning differently.

Some people like detailed conversations and regular check-ins. Others prefer a quieter, more gradual approach.

There’s no single “right way” to plan.

For many, especially those who are more private or reflective, it’s important that financial planning happens at a pace that feels comfortable — without pressure or urgency.

The process should adapt to you, not the other way around.

What’s Important to You?

At the centre of financial planning is a simple question:

What’s important to you?

Not what the market is doing.

Not what someone else is prioritizing.

Not what you feel like you “should” be doing.

Just you.

Whether that means:

The role of financial planning is to support those priorities in a way that feels clear and achievable.

A Place to Start — Without Pressure

If you’ve been thinking about financial planning but haven’t been sure where to begin, that’s okay.

You don’t need to have everything figured out.

You don’t need to be at a certain stage.

You don’t need to feel “ready.”

If you’d like to have a conversation about where you are and where you’d like to go, you’re always welcome to reach out.

No pressure — just a place to start.

When you sign your mortgage documents, there’s often a moment where you’re offered mortgage insurance through the bank. It can feel convenient. Simple. Almost automatic.

But it’s important to pause and ask a gentle question:

Who is this coverage truly protecting?

This conversation has come up more often lately, especially following Doug’s recent thoughts on ManuOne and ownership. And I think it’s an important one — because protection should always be centred around your family.

The Key Difference: Who Benefits?

Bank mortgage insurance is designed to pay off your mortgage directly to the lender if something happens to you.

That means the bank receives the funds.

Your family receives a mortgage-free home — which can certainly help — but they do not receive control over the money itself.

With personally owned life insurance, it’s very different.

You:

If something happens, the benefit is paid directly to the people you love. They can use it to pay off the mortgage, replace income, cover education costs, or manage day-to-day living expenses.

Personal insurance protects your family.

Mortgage insurance protects the bank.

That distinction matters.

Underwriting: When It Happens Makes a Difference

Another important difference is when the underwriting occurs.

With personally owned life insurance, underwriting is completed upfront, when you apply. You know you’re approved. You know the terms. There are no surprises later.

With many bank mortgage insurance policies, underwriting is often completed at the time of claim. This can result in delays — and in some cases, even denial of the claim if something in your health history raises questions.

In a time of grief, your family should not be navigating uncertainty.

Clarity and certainty bring peace of mind.

Cost and Flexibility

Many people are surprised to learn that personally owned life insurance can:

Bank mortgage insurance is typically tied to your mortgage balance — meaning as your mortgage decreases, your coverage decreases, but your premium often stays the same.

With personal coverage, your protection amount remains consistent for your loved ones.

Protection Should Reflect What’s Important to You

At YourStyle Financial, we believe insurance isn’t about paperwork — it’s about people.

It’s about ensuring your family has options, stability, and breathing room during a difficult time.

Mortgage insurance may feel convenient. Personally owned life insurance feels intentional.

If you’re unsure what you currently have, or if you’ve never compared the two, I’m always happy to sit down and review it with you. There’s no pressure — just clarity.

Because protection should always be built around what’s important to you.

— Samantha

For many people, the idea of meeting with a financial advisor can feel intimidating.

You might wonder:

If any of those thoughts feel familiar, you’re not alone. Many people in Manitoba delay financial planning simply because they aren’t sure what the experience will actually be like.

The reality is, working with a financial advisor doesn’t need to feel overwhelming or uncomfortable. When done properly, it should feel steady, clear, and centred around one simple question:

What’s important to you?

Why Financial Advisors Can Feel Intimidating

There are a few common reasons people hesitate to reach out:

If you’ve ever felt that way, it’s completely understandable.

Financial planning is personal. It involves your goals, your habits, your priorities, and sometimes your uncertainties. It should never feel like an interrogation or a performance review.

What Working With a Financial Advisor at YourStyle Actually Looks Like

The process is simpler than many people expect.

1. It Starts With a Conversation — Not a Presentation

The first meeting isn’t about charts or projections.

It’s about understanding you.

There’s no pressure to have everything prepared. You don’t need to “know enough.” The goal is simply to start a conversation in a way that feels comfortable.

2. Clarity Before Complexity

Financial planning doesn’t need to be complicated to be effective.

Rather than overwhelming you with terminology or technical details, the focus is on helping you understand what matters most and what steps make sense next.

That might include:

The pace is steady and thoughtful. Questions are always welcome.

3. A Comfortable, Judgment-Free Environment

Many people worry they’ll be told they should have started sooner, saved more, or structured things differently.

That’s not helpful.

Everyone’s path looks different. Life happens. Careers change. Families grow. Priorities evolve.

Financial planning should meet you where you are — not where someone thinks you “should” be.

The goal is to create clarity and confidence, not pressure.

4. Ongoing Support That Reflects Your Comfort Level

Some clients prefer regular check-ins. Others prefer fewer meetings with time to reflect between conversations.

There isn’t a single “right” way to plan.

The process adapts to your personality, your pace, and your preferences. For those who are naturally more introverted or private, planning can be structured in a way that feels calm and manageable.

Financial planning should fit into your life — not take it over.

What’s Important to You?

At the end of the day, financial planning isn’t about outperforming markets or chasing complexity.

It’s about helping you make decisions that support what matters most in your life.

Whatever that looks like for you, it starts with a conversation.

If you’ve been feeling hesitant or unsure about what working with a financial advisor looks like, know that it doesn’t need to feel intimidating.

If you’d like to learn more about the process or simply have an initial conversation, you’re always welcome to reach out. There’s no pressure — just a place to begin.

Getting married is an exciting step — one that comes with new conversations, shared goals, and a future you’re beginning to shape together. Alongside planning a wedding or settling into life as a couple, many people start thinking about finances and wonder where to begin.

(more…)Part 7 of 7 | Financial Wellness Series

In the final episode of our Financial Wellness Video Series, Doug Buss, founder of YourStyle Financial, joins Rafiq Punjani from Right at Home to discuss how thoughtful tax planning can help families keep more of what they’ve earned — while also supporting the causes that matter most to them.

(more…)

Part 5 of 7 | Financial Wellness Series

In the fifth episode of our Financial Wellness Video Series, Doug Buss, founder of YourStyle Financial, joins Rafiq Punjani from Right at Home to discuss some of the most common mistakes families and private caregivers make — and how to navigate those challenges with financial awareness and compassion.

(more…)

Part 4 of 7 | Financial Wellness Series

In the fourth episode of our Financial Wellness Video Series, Doug Buss, founder of YourStyle Financial, joins Rafiq Punjani from Right at Home to talk about how to provide meaningful support for elders who are beginning to need help — while maintaining their independence, confidence, and dignity.

(more…)

Part 3 of 7 | Financial Wellness Series

In the third installment of our Financial Wellness Video Series, Doug Buss, founder of YourStyle Financial, joins Rafiq Punjani from Right At Home to talk about what happens when someone reaches out for help because they’re struggling financially — particularly later in life.

(more…)

Part 1 of 7 | Financial Wellness Series

In this first installment of our Financial Wellness Video Series, Doug Buss, founder of YourStyle Financial, sits down with Rafiq Punjani from Right At Home to talk about the real financial challenges adults — especially retirees — are facing today.

With inflation driving up the cost of everyday goods and services, many Canadians living on a fixed income are finding it increasingly difficult to maintain the lifestyle they once enjoyed. Doug explains how YourStyle Financial works closely with clients to understand where their money is going, identify opportunities to make changes, and help them use their income and investments more efficiently.

“It’s about helping people make informed decisions,” says Doug. “When interest rates are at 40-year lows, those who rely on investment income — particularly seniors — are often hit the hardest. Our job is to help them adjust, plan, and still find ways to enjoy life.”

This episode highlights the importance of personalized financial planning, proactive budgeting, and creative strategies to maximize income, even in a challenging economic climate.

🎥 Watch the full video below to hear Doug’s insights and practical advice.

📆 This is Part 1 of our 7-part Financial Wellness Series. Be sure to check back every week for a new episode featuring helpful discussions about financial planning, investments, and real-world solutions to help you live the life you deserve.

Are you dreaming of owning your first home? YourStyle Financial, a compassionate and understanding financial planning organization in Winnipeg, is here to help you make that dream a reality.

In their latest video, Doug Buss introduces the First Home Savings Plan, a powerful tool designed to help first-time homebuyers save efficiently. YourStyle Financial’s expertise ensures that you can navigate the complexities of financial planning with ease. Their personalized approach and dedication to understanding what’s important to you make them a trusted partner on your journey to homeownership.

Watch the full video on YourStyle Financial’s Media Page to learn more about the First Home Savings Plan and start your journey towards homeownership today.

(more…)

When it comes to planning for the future, it’s never too early to start. At YourStyle Financial, we believe in the power of proactive planning to ensure that you and your loved ones are prepared for any eventuality. One crucial aspect of this planning is understanding and arranging a Power of Attorney (POA).

Why Plan Now?

Life is unpredictable. Whether it’s an unexpected illness, accident, or simply the progression of age, having the right documents in place can make all the difference. Waiting until things go wrong can lead to unnecessary stress and complications, especially when it comes to managing finances and healthcare decisions.

(more…)

At YourStyle Financial, we believe in the power of whole-life management. Based in Winnipeg, our mission is to prioritize “What’s Important To You”. Here’s how we bring family-focused financial planning to life.

The Importance of Family Meetings

Financial planning is more than just numbers; it’s about family dynamics, communication, and legacy. Family meetings can help navigate these complex relationships, ensuring everyone’s voice is heard and respected.

(more…)

The team at YourStyle Financial is excited to see Doug in the news again. This time the Free Press has highlighted Doug’s extensive career serving clients in Winnipeg.

As Joel Schlesinger states “Then it might come as a surprise that the veteran has only recently received the Distinguished New Advisor of the Year Award, for 2022.”. Anyone who’s even spoken with Doug knows this award acknowledges everything he stands for.

“So while Buss may be an experienced certified financial planner, his most recent accomplishment and the accompanying award speak to the fact he never stops learning.”

Continuous growth and advancement are a point of pride for Doug and the YourStyle team.

Here is the link to the full article and we would love for you to read it. :

If you’d like to experience Doug’s knowledge and experience to determine “What’s Important to You?”, we would love to help you with all of your financial planning needs. Contact us today.

For many, the last two years have made a lot of people more attentive to two things; money and mortality – both of which are the pinnacle of adulting. They’re also both the two things no one likes to think about. For most, there’s not enough of either money or time. But when the time comes, will there be enough money?

If you’re evaluating your accounts and expenditures and deciding where you can cut costs, are you wondering if your life insurance policy is worth the monthly premiums? Is it a necessary expense? Is it something you need and why? Let’s explore those questions.

(more…)

Today’s environment has changed the employment market significantly. While Manitoba has one of the highest unemployment rates of recent history, it is still the employees market. Government subsidies have made it easier for some to opt to stay home leaving many open positions and therefore choices for those who are continuing to work. With that it falls back on the employer to be competitive and offer incentives to work at their company and stay working there. One of those offerings are Group Benefit Plans. If you’re a business owner, you’ve probably wondered “is now the right time to add group benefits?”. Here are a few points to help guide your decision:

(more…)