The Hidden Cost of “Doing Nothing” With Your Money

It’s something I hear often:

“At least my money is safe in the bank.”

And I understand where that comes from.

There’s comfort in knowing your savings aren’t going up and down with the markets.

But what’s often missed is this:

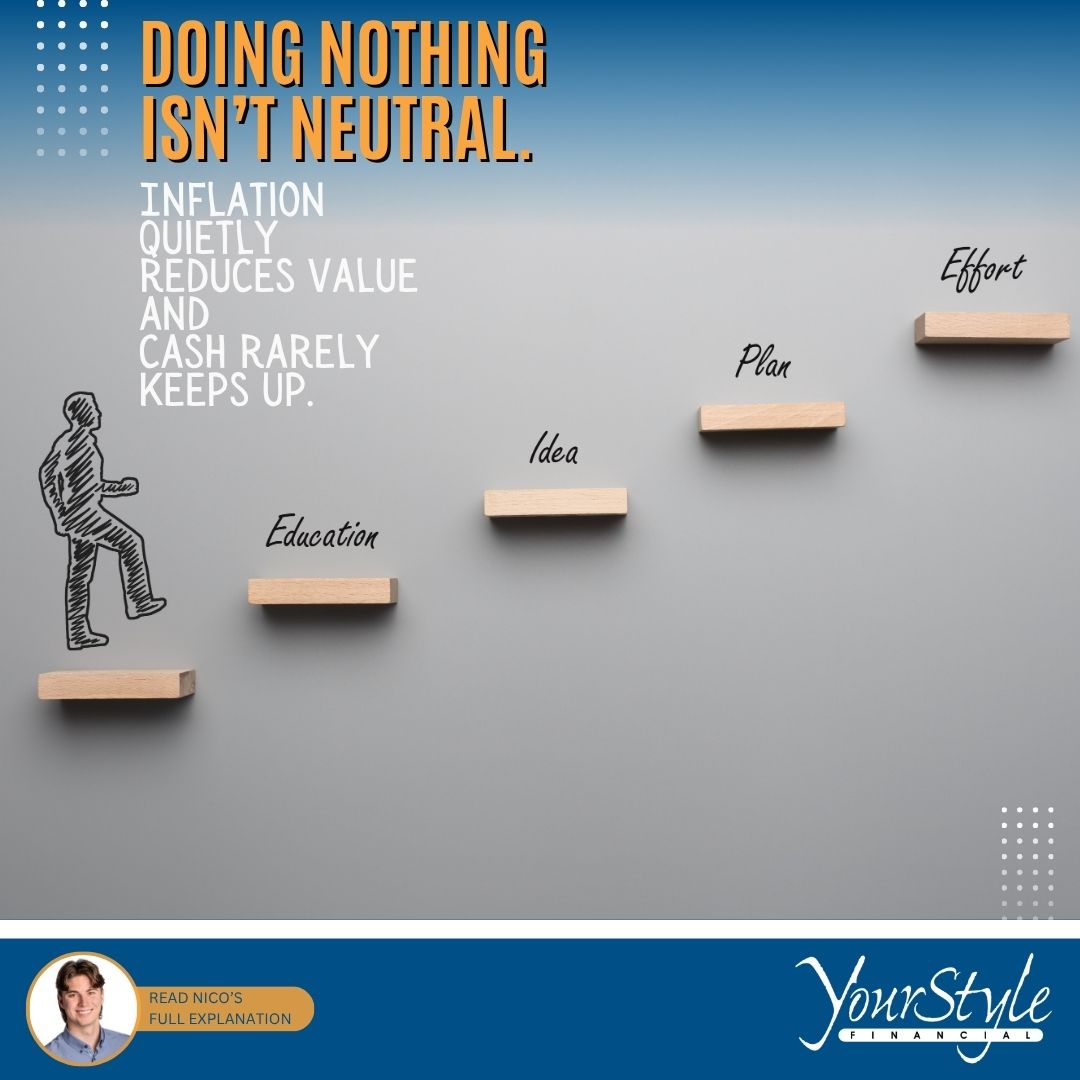

Doing nothing with your money isn’t neutral.

Over time, it can quietly cost you more than you think.

Inflation Is Always Working in the Background

Even when inflation feels “low” — say 2–3% — it’s still reducing what your money can actually do for you over time.

A simple way to think about it:

- $50,000 today does not equal $50,000 worth of lifestyle in the future

- The cost of everyday things — groceries, fuel, housing — gradually increases

- Your money, if it’s sitting still, does not keep up

Nothing dramatic happens overnight.

But over years, the difference becomes meaningful.

The Opportunity Cost of Staying in Cash

Keeping money in a savings account might feel like the safest choice — but there’s a trade-off.

Historically:

- Long-term market returns have averaged roughly 6–10% annually

- Savings accounts often return 1–2% (if that)

That gap matters more than most people realize.

Here’s a simple example:

- $10,000 invested at 7% for 25 years → ~$54,000

- $10,000 in cash at 2% for 25 years → ~$16,400

That’s not about taking unnecessary risk — it’s about understanding what happens when money doesn’t grow.

Time Is the Most Valuable Asset You Have

One of the biggest advantages anyone can have financially is simply starting earlier.

Even small amounts can make a significant difference over time.

To put this into perspective, here’s an example assuming a 7% annual rate of return over the long term:

Example:

Scenario A: Start Small, Then Increase Later

- $50/month from age 25–35 (10 years)

- Then $300/month from age 35–65 (30 years)

Results:

- Total contributed: $114,000

- Final value at 65: ~$435,000

Scenario B: Wait, Then Invest More

- $0 from age 25–35

- Then $300/month from age 35–65

Results:

- Total contributed: $108,000

- Final value at 65: ~$365,000

These are hypothetical examples for illustration purposes, and actual returns will vary.

Even though the contributions are similar, the earlier start leads to a noticeably different outcome.

Not because of how much was invested — but because of time.

It’s Not About Taking Big Risks

This isn’t about putting everything into the market or making aggressive decisions.

It’s about balance.

- Keeping some money accessible

- Letting some money grow

- Having a plan that reflects your comfort level and goals

For many people, the biggest risk isn’t volatility — it’s falling behind quietly without realizing it.

Final Thoughts

If your money is sitting in a savings account, you’re not doing anything wrong.

But it’s worth asking:

Is this working as well as it could for me?

Financial planning isn’t about pressure or quick decisions.

It’s about understanding your options and making choices that feel right for you.

If you ever want to talk it through — even just as a second opinion — I’m always happy to listen.